Over the past year we have released numerous articles about credit scores, detailing what a credit score is, what a bad credit score looks like, how to check your score and how to improve it. But did you know you actually have several credit scores?

There are multiple credit referencing agencies in the UK, each providing you with a report of your credit history and each coming with their own methods or scale on which to score you. Most of us have heard of “bad” and “good” credit, but the lesser spoken about “average credit” still exists, and if that’s where you are, you might be curious to know where you fit on the scale.

As there are several agencies that provide credit scores, it also means there’s no such thing as a universal average credit score. However, within each credit agency’s scoring matrix there is a general truth – the higher the number, the better – and a higher number often comes with better chances of getting a mortgage approval (furthermore- better rates).

Even so, it’s still important to note that a good score from a credit reference agency is no guarantee your application will be successful as the lender takes many other factors into account- such as affordability and conduct of your bank account.

Is there an average credit score?

Your credit score is the number that tells lenders how reliable you are when it comes to repaying debt. However, as mentioned above – there isn’t just one universal credit score. There are three main credit reference agencies in the UK that lenders use to check your credit report, all of which have different score ranges. As such, there is an average score for each agency, but not an average credit score overall.

How is a credit score calculated?

Each credit reference agency has their own method, scale and criteria when it comes to calculating your credit score, but generally there are multiple factors;

- The number of accounts – as with many things, less is more. A few, well managed accounts often trump many open credit accounts.

- Types of accounts

- The use of your available credit – this refers to your credit limit and how much you are using. If you’re using most of or maxing out your credit limit, this could lower your score.

- The length of your history – if you’ve never taken out credit, there will be little data on how you manage repayments, and therefore little data to score on. A longer history gives more information, providing a more accurate calculation that reflects your borrowing habits.

- Your payment history – how you’ve handled your repayments over time. If you’ve kept your account payments up to date and kept an eye on your finances, then your credit score should reflect this. Late or missed payments, and the marks that follow if not resolved, will also appear and could reduce your score.

The information each reference agency might have about you can vary as lenders/account providers may only report to one, two or none of the agencies.

The main credit reference agencies are Equifax, Experian and TransUnion, and it’s worth checking all three if you’re looking to get the most in-depth picture of what potential lenders might see.

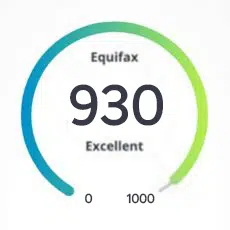

Equifax Credit Score:

The Equifax scale ranges from 0 to 1000 with the average rate being around 380*.

Equifax credit score range:

Equifax credit score range:

- Poor: 0-438

- Fair: 439-530

- Good: 531-670

- Very Good: 671-810

- Excellent: 811-1000

Average rate was based on the old score of 700

Experian Credit Score:

The maximum Experian credit score is 999 and the average score among its customers is 759 – which is rated as a ‘fair’ credit score.

Experian credit score range:

Experian credit score range:

- Very Poor: 0-560

- Poor: 561-720

- Fair: 721-880

- Good: 881-960

- Excellent: 961-999

TransUnion Credit Score:

TransUnion rate your credit score out of 710 and the average score amongst their customers is 610.

![]() TransUnion credit score range:

TransUnion credit score range:

- Very Poor: 0-550

- Poor: 551-565

- Fair: 566-603

- Good: 604-627

- Excellent: 628-710

Average UK scores:

Experian (who score out of 999) released the average credit scores by location.

Sheffield – 773

Peterborough – 755

Newcastle – 761

Nottingham – 745

Cambridge – 836

Cardiff – 770

Bristol – 833

Oxford – 811

Glasgow – 767

You can find out what the average credit score is for where you live by heading over here.

What do lenders class as a ‘good’ score?

Taking the wide variety of scoring systems and the vast difference in maximum scores for each reference agency into account, you can see why a universal average would be so difficult to calculate. As such, lenders often take information from all of the referencing agencies, and blend it to get the data they need to make their decision.

Each agency has their own definition of a “good” score:

Equifax – 531 +

Experian – 881+

TransUnion – 604 +

Out of all three major credit referencing agencies, only TransUnion has their average score in the ‘good credit’ category, with Equifax finding their average as ‘poor’ and Experian’s average being ‘fair’.

Clever Mortgages are specialists in finding mortgages for clients with a low credit score, and for those who have struggled financially in the past. We can offer a free credit report -which won’t affect your score- to help them to find the best lender for your financial situation.

How can I improve my credit score?

Regardless of where you are on your journey to applying for a mortgage and securing a home, it’s worth taking steps to improve your credit score. This will improve your chances of being approved for a better mortgage, as well as other financial products in the future.

Ways to improve your credit score include:

- Pay your bills and accounts on time, create a budgeting plan if needed and set up direct debits to keep things punctual

- Keep your credit card balances below 30% of your total credit limit. Even better, keep them below 10%

- Close any unused accounts

- Make sure you are registered on the electoral roll

- If your credit score is low or you have a limited credit history, it could be worth looking into a well-managed credit card or phone contract to help boost your score

- Avoid making several credit applications in a short span of time- hard searches can impact your score.

If you are looking for a lender, soft searches can be done by our brokers at Clever Mortgages to get an idea of which lenders will be most likely to accept your application before you submit it

Time heals all, and the same goes with your credit- marks usually drop off after 6 years, and the more time that passes since said marks, the better a lender views it. If you keep up with your repayments, keep an eye on your credit reports and work to maintain your financial health you’ll see vast improvements in your score.

If you’ve just started searching for properties or have found your dream home but are struggling to find a mortgage, let the team at Clever Mortgages guide you through the process. You can start your journey by visiting www.clever-mortgages.co.uk or give us a call today on 0330 232 0285.

*Data supplied by helpandadvice September 2021.